When recording artist Prince got into a contract dispute with his record label, Warner Brothers, he literally changed his name to an unpronounceable symbol and was thereafter referred to as The Artist Formerly Known As Prince.

Which brings us to The Platform Currently Known As Facebook, which will soon be a name to forget, with a nod to those readers among you for whom that ship sailed long ago, name change or not.

As a writer, we love words. New words enter the patois constantly, and always good to keep up, what, eh? Some we appreciate; some leave us utterly gobsmacked. You needed to turn that noun into a verb? Seriously??? Sometimes they make sense. Ofttimes, we roll our eyes at the absurdity. Those are the ones that we know in our heart of hearts will lead us right down the rabbit hole

We thought we’d share a few that have entered the vocabulary, for better or for worse:

Facebook, Whatsapp, Instagram, Messenger and Oculus – all Facebook-owned properties – all went offline Monday, and odd that the outage came the day/morning after the “60 Minutes” interview with former Facebook employee turned whistleblower Frances Haugen.

“The documents, first reported in a series of (Wall Street) Journal stories, revealed that the company’s executives understood the negative impacts of Instagram among younger users and that Facebook’s algorithm enabled the spread of misinformation, among other things,” CNBC reported.

In the 60 Minutes interview, Haugen said, among other things, that Facebook is “tearing our societies apart and is causing ethnic violence around the world.”Read More...

When the tech industry was first establishing itself, it was something completely new to the planet, like, for example, the Industrial Age before it. Various mantras hit the zeitgeist: fake it til you make it; move fast and break things; fail fast. There are byproducts of these practices: the disregard for ethics, morality and responsibility or as we’ve said many times before, the only way to cover up a crime is to commit an even bigger crime.

The Elizabeth Holmes trial is on and it turns out that the Stanford dropout sidelined the real scientists at Theranos “By leaving them off email threads,” The Verge reported. Then attempted to blame them for Theranos’s failures. “A lot of new emails were introduced, showing Holmes was aware of the company’s problems, and was even actively trying to manage the situation. Several times in those emails, (former Theranos lab director Adam) Rosendorff tried to get Theranos labs to run FDA-approved tests instead of the ones Theranos developed. But maybe even more telling were the emails that Rosendorff was excluded from…“The company was more about PR and fundraising than patient care,” he said.Read More...

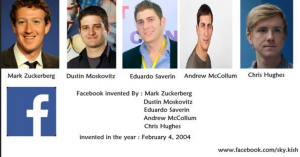

Mark Zuckerberg was back on Capitol Hill last week, testifying before Congress about the proposed cryptocurrency, Libra.

“I don’t control Libra” was the central theme of the Facebook CEO’s testimony,” according to TechCrunch. “The House of Representatives unleashed critiques of his approach to cryptocurrency, privacy, encryption and running a giant corporation during six hours of hearings. Zuckerberg tried to assuage their fears while stoking concerns that if Facebook doesn’t build Libra, the world will end up using China’s version.”Read More...

More and more we’re seeing founders without so much as a plan to profitability raise outrageous amounts of venture capital based mostly on, from what we can tell, hubris, being mediagenic and what may arguably be either a Napoleonic complex, a touch of bipolar syndrome, or some combination of the two.

There seems to be a clear pathway to success in technology without having to be bothered with showing profits or even having a viable or clearly defined product, but given the downfall of Elizabeth Holmes (Theranos), Travis Kalanick (Uber), and most lately Adam Neumann (WeWork), that pathway hasn’t been clearly defined, or refined. But we have been paying attention, and we believe we have come up with 12 basic rules for success in technology – even with little or simple tech required:Read More...

Facebook announced the soon-to-debut of Libra, its new cryptocurrency, last week, saying that it hoped to bring billions of the unbanked into the digital economy, providing them with basic financial services through their cellphones, eerily echoing Facebook’s original mission to bring the world closer together with its social platform, in case you missed the irony.

Now that the LUPA/PAUL stocks have (mostly) gone public – Lyft, Uber, Pinterest and Airbnb), these supposed category killers aren’t exactly killing it in the stock market. It’ll be interesting to see how the massively funded We Company (nee WeWork) does and despite all of this, we’re still witnessing massive funding rounds. Vice, for one, despite its stalled growth, recently raised $250M, a pittance compared to the $575M raised by Deliveroo. At some point, growth does stall; hockey stick growth is unsustainable or as Douglas Rushkoff, author of Team Human et al, said at the Techonomy conference in New York last week, “exponential growth is a problem. The only thing that can grow exponentially forever is cancer, and then it kills its host.”

We’ve known Rushkoff personally since the early days of Web 1.0, which, he reminded us, was when we all innocently believed that the web would distract us from the insular world of television and bring us together, which Mark Zuckerberg told Congress was the intention of Facebook. Well, that and world domination, although he did not share the latter with Congress.

Back in those early days, Wired Magazine told us that the internet was going to be the salvation of the NASDAQ stock exchange. This was the attention economy, and, said Wired, thanks to digital, the economy would grow exponentially, unstopped, forever. And Alan Greenspan agreed: New paradigm! Unlimited growth! Forever! What they didn’t realize was that this economic system was a very old, obsolete operating system invented by the monarchs in the 12th and 13th century to prevent the rise of the middle class, Rushkoff noted.Read More...

If you’ve ever applied to an accelerator or approached (many) investors for funding, one of the most important points they check, especially in the case of investors, is team.

Above all, they want to know about the co-founders, and truth be told, most investors shy away from a startup with a solitary founder, the stated reason most often being that you should be able to find at least one person who shares your vision or passion and is willing to throw in with you. It’s also difficult to operate in a vacuum: much easier if you have that other person off whom to bounce ideas, and to keep you in check, if need be.Read More...